Filed by Bowne Pure Compliance

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| |

|

|

| þ |

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the fiscal year ended December 29, 2007.

OR

| |

|

|

| o |

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period of to .

Commission File No.: 0-22684

UNIVERSAL FOREST PRODUCTS, INC.

(Exact name of registrant as specified in its charter)

| |

|

|

| Michigan

|

|

38-1465835 |

| (State or other jurisdiction of

|

|

(I.R.S. Employer |

| incorporation or organization)

|

|

Identification No.) |

| |

|

|

| 2801 East Beltline, N.E., Grand Rapids, Michigan

|

|

49525 |

| (Address of principal executive offices)

|

|

(Zip Code) |

Registrant’s telephone number, including area code (616) 364-6161

Securities registered pursuant to Section 12(b) of the Act:

| |

|

|

| Title Of Each Class |

|

Name of Each Exchange on Which Registered |

| None |

|

|

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, no par value

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of

the Securities Act.

Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or

Section 15(d) of the Act.

Yes o No þ

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by

Section 13, or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for

such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements in the past 90 days.

Yes þ No o

Indicate

by check mark if disclosure of delinquent filers pursuant to Items 405 of Regulation S-K is

not contained herein, and will not be contained, to the best of registrant’s knowledge, in

definitive proxy or information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated

filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large

accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act. (Check one):

| |

|

|

|

|

|

|

| Large accelerated filer þ |

|

Accelerated filer o |

|

Non-accelerated filer o

(Do not check if a smaller reporting company) |

|

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12-2 of the Act.)

Yes o No þ

The aggregate market value of the common stock held by non-affiliates of the registrant (i.e.

excluding shares held by executive officers, directors, and control persons as defined in Rule 405,

17 CFR 230.405) on June 30, 2007 was $661,771,865 computed at the closing price of $42.26 on that

date.

As of February 2, 2008, 18,922,136 shares of the registrant’s common stock, no par value, were

outstanding.

Documents incorporated by reference:

| (1) |

|

Certain portions of the registrant’s Annual Report to Shareholders for the fiscal year ended

December 29, 2007 are incorporated by reference into Part I and II of this Report. |

| (2) |

|

Certain portions of the registrant’s Proxy Statement for its 2008 Annual Meeting of

Shareholders are incorporated by reference into Part III of this Report. |

Exhibit Index located on page E-1.

ANNUAL REPORT ON FORM 10-K

December 29, 2007

TABLE OF CONTENTS

2

PART I

Item 1. Business.

General Development of the Business.

Universal Forest Products, Inc. was organized as a Michigan corporation in 1955. We engineer,

manufacture, treat, distribute and install lumber, composite wood, plastic and other building

products to the do-it-yourself/retail (“DIY/retail”), site-built construction, manufactured

housing, and industrial markets. We currently operate facilities throughout the United States,

Canada, and Mexico.

Information relating to current developments in our business is incorporated by reference from our

Annual Report to Shareholders for the fiscal year ended December 29, 2007 (“2007 Annual Report”)

under the caption “Management’s Discussion and Analysis of Financial Condition and Results of

Operations.” Selected portions of the 2007 Annual Report are filed as Exhibit 13 with this Form

10-K Report.

Financial Information About Segments.

Statement of Financial Accounting Standards (“SFAS”) No. 131, Disclosures about Segments of an

Enterprise and Related Information (“SFAS 131”) defines operating segments as components of an

enterprise about which separate financial information is available that is evaluated regularly by

the chief operating decision maker in deciding how to allocate resources and in assessing

performance. Under the definition of a segment, our Eastern, Western and Consumer Products

Divisions may be considered an operating segment of our business. Under SFAS 131, segments may be

aggregated if the segments have similar economic characteristics and if the nature of the products,

distribution methods, customers and regulatory environments are similar. We have aggregated our

Eastern and Western divisions into one reporting segment, consistent with SFAS 131. Our Consumer

Products Division, which was formed in 2006, is included in “All Other.” Separate Financial

information about industry segments is incorporated by reference from Note O of the Consolidated

Financial Statements presented under Item 8 herein.

Narrative Description of Business.

We presently engineer, manufacture, treat, distribute and install lumber, composite wood, plastic

and other building products for the DIY/retail, site-built construction, manufactured housing, and

industrial markets. Each of these markets is discussed in the paragraphs which follow.

DIY/Retail Market. The customers comprising this market are primarily national home center

retailers, retail-oriented regional lumberyards and contractor-oriented lumberyards. Generally,

terms of sale are established for annual periods, and orders are placed with our regional

facilities in accordance with established terms. One customer, The Home Depot, accounted for

approximately 26% of our total net sales for fiscal 2007, 22% for 2006, and 22% for 2005.

3

From time to time we enter into certain sales contracts with The Home Depot. The contracts are

limited to the establishment of general sales terms and conditions, such as delivery, invoicing,

warranties and other standard, commercial matters. Sales are made by the release of purchase

orders to us for particular quantities of certain products. We also enter into marketing

agreements and rebate agreements with The Home Depot. The marketing agreements provide a certain

percentage of our sales revenue or a minimum dollar amount will be committed to generate sales for

us and The Home Depot.

We currently supply customers in this market from many of our locations. These regional facilities

are able to supply mixed truckloads of products which can be delivered to customers with rapid

turnaround from receipt of an order. Freight costs are a factor in the ability to competitively

service this market, especially with treated wood products because of their heavier weight. The

close proximity of our regional facilities to the various outlets of these customers is a

significant advantage when negotiating annual sales programs.

The products offered to customers in this market include dimensional lumber (both preserved and

unpreserved) and various “value-added products,” some of which are sold under our trademarks. In

addition to our conventional lumber products, we offer composite wood and plastic products. We

also sell engineered wood products to this market, which include roof trusses, wall panels and

engineered floor systems (see “Site-Built Construction Market” below).

We are not aware of any competitor that currently manufactures, treats and distributes a full line

of both value-added and commodity products on a national basis. We face competition on individual

products from several different producers, but the majority of these competitors tend to be

regional in their efforts and/or do not offer a full line of outdoor lumber products. We believe

the breadth of our product offering, geographic dispersion, customer relationships, close proximity

of our plants to core customers, purchasing and manufacturing expertise and service capabilities

provide significant competitive advantages in this market.

Site-Built Construction Market. We entered the site-built construction market through

strategic business acquisitions. The residential housing customers comprising this market are

primarily large-volume, multi-tract builders and smaller volume custom builders. We also supply

builders engaged in multi-family and commercial construction. Generally, terms of sale and pricing

are determined based on quotes for each order.

We currently supply customers in this market from manufacturing facilities located in many

different states and Canada. These facilities manufacture various engineered wood components used

to frame residential or commercial projects, including roof and floor trusses, wall panels, Open

Joist 2000®, I-joists and lumber packages. Freight costs are a factor in the ability to

competitively service this market due to the space requirements of these products on each

truckload.

4

We also provide framing services for customers in certain regional markets, in which we erect the

wood structure. We believe that providing a comprehensive framing package, including installation,

provides a competitive advantage. Terms of sale are based on a construction contract.

Competitors in this market include national and regional retail contractor yards who also

manufacture components and provide framing services, as well as regional manufacturers of

components. Our objective is to continue to increase our manufacturing capacity and framing

capabilities for this market while developing a national presence. We believe our primary

competitive advantages relate to the engineering and design capabilities of our regional staff,

customer relationships, purchasing and manufacturing expertise, product quality and timeliness of

delivery.

Manufactured Housing Market. The customers comprising the manufactured housing market are

producers of mobile, modular and prefabricated homes and recreational vehicles. Products sold to

customers in this market consist primarily of roof trusses, lumber cut and shaped to the customer’s

specification, plywood, particle board and dimensional lumber, all intended for use in the

construction of manufactured housing. Sales are made by personnel located at each regional

facility based on customer orders.

Our principal competitive advantages include our customer relationships, product knowledge, the

strength of our engineering support services, the close proximity of our regional facilities to our

customers, our purchasing and manufacturing expertise and our ability to provide national sales

programs to certain customers. These factors have enabled us to accumulate significant market

share in the products we supply.

Industrial Market. We define our industrial market as industrial manufacturers and

agricultural customers who use pallets, specialty crates and wooden boxes for packaging, shipping

and material handling purposes. Many of the products sold to this market may be produced from the

by-product of other manufactured products, thereby allowing us to increase our raw material yields

while expanding our business. Competition is fragmented and includes virtually every supplier of

lumber convenient to the customer. We service this market with our dedicated local sales teams and

national sales support efforts, combined with our competitive advantages in manufacturing,

purchasing, and material utilization.

Suppliers. We are one of the largest domestic buyers of solid sawn lumber from primary

producers (lumber mills). We use primarily Southern Yellow Pine in our pressure-treating

operations and site-built component plants in the Southeastern United States, which we obtain from

mills located throughout the states comprising the Sunbelt. Other species we use include

“spruce-pine-fir” from various provinces in Canada; hemlock, Douglas fir and cedar from the Pacific

Northwest; inland species of pine, plantation grown radiata and southern yellow pines from South

America; and European spruce. There are numerous primary producers for all varieties we use, and

we are not dependent on any particular source of supply. Our financial resources and size, in

combination with our strong sales network and ability to remanufacture

lumber, enable us to

purchase a large percentage of a primary producer’s output, (as opposed to only those dimensions or

grades in immediate need), thereby lowering our average cost of raw materials and allowing us to

obtain programs such as consigned inventory. We believe this represents a competitive advantage.

5

Intellectual Property. We own several patents and have several patents pending on

technologies related to our business. In addition, we own numerous registered trademarks and claim

common law trademark rights to several others. As we develop proprietary brands, we may pursue

registration or other formal protection. While we believe our patent and trademark rights are

valuable, the loss of a patent or any trademark would not be likely to have a material adverse

impact on our competitive position.

Backlog. Due to the nature of our DIY/retail, manufactured housing and industrial

businesses, backlog information is not meaningful. The maximum time between receipt of a firm

order and shipment does not usually exceed a few days. Therefore, we would not normally have a

backlog of unfilled orders in a material amount. The relationships with our major customers are

such that we are either the exclusive supplier of certain products and/or certain geographic areas,

or the designated source for a specified portion of the customer’s requirements. In such cases,

either we are able to forecast the customer’s requirements or the customer may provide an estimate

of its future needs. In neither case, however, will we receive firm orders until just prior to the

anticipated delivery dates for the products in question.

On December 29, 2007 and December 30, 2006, we estimate that backlog orders associated with the

site-built construction business approximated $101.6 million and $119.8 million, respectively.

With respect to the former, we expect that these orders will be primarily filled within the current

fiscal year, however, it is possible that some orders could be canceled.

Environmental. Information required for environmental disclosures is incorporated by

reference from Note M of the Consolidated Financial Statements presented under Item 8 herein.

Seasonality. Information required for seasonality disclosures is incorporated by reference

from Item 1A. Risk Factors under the caption “Seasonality and weather conditions could adversely

affect us.”

Employees. On December 29, 2007, we had approximately 8,400 employees.

Financial Information About Geographic Areas.

The dominant portion of our operations and sales occur in the United States. Separate financial

information about foreign and domestic operations and export sales is incorporated by reference

from Note O of the Consolidated Financial Statements presented under Item 8 herein.

6

Available Information.

Our Internet address is www.ufpi.com. Through our Internet website under “Financial Information”

in the Investor Relations section, we make available free of charge, as soon as reasonably

practical after such information has been filed with the SEC, our annual report on Form 10-K,

quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed

pursuant to Section 13(a) or 15(d) of the Securities Exchange Act. Also

available through our Internet website under “Corporate Governance” in the Investor Relations

section is our Code of Ethics for Senior Financial Officers.

Reports to Security Holders.

Not applicable.

Enforceability of Civil Liabilities Against Foreign Persons.

Not applicable.

Item 1A. Risk Factors.

We are subject to fluctuations in the price of lumber. We experience significant fluctuations in

the cost of commodity lumber products from primary producers (the “Lumber Market”). A variety of

factors over which we have no control, including government regulations, environmental regulations,

weather conditions, economic conditions, and natural disasters, impact the cost of lumber products

and our selling prices. While we attempt to minimize our risk from severe price fluctuations,

substantial, prolonged trends in lumber prices can negatively affect our sales volume, our gross

margins, and our profitability. We anticipate that these fluctuations will continue in the future.

Our growth may be limited by the markets we serve. Our sales growth is dependent, in part, upon

the growth of the markets we serve. If our markets do not achieve anticipated growth, or if we

fail to maintain our market share, financial results could be impaired.

Our ability to achieve sales and margin goals, particularly on sales to the site-built construction

market, is impacted by housing starts. If housing starts decline significantly, our financial

results could be negatively impacted. Single-family housing starts fell approximately 29% in 2007

compared to 2006.

We are witnessing consolidation by our customers in each of the markets we serve. These

consolidations will result in a larger portion of our sales being made to some customers and may

limit the customer base we are able to serve.

7

A significant portion of our sales are concentrated with one customer. Our sales to The Home Depot

comprised 26% of our total sales in 2007, 22% in 2006, and 22% in 2005.

Our growth may be limited by our ability to make successful acquisitions. A key component of our

growth strategy is to complete business combinations. Business combinations involve inherent

risks, including assimilation and successfully managing growth. While we conduct extensive due

diligence and have taken steps to ensure successful assimilation, factors beyond our control could

influence the results of these acquisitions.

We may be adversely affected by the impact of environmental and safety regulations. We are subject

to the requirements of federal, state, and local environmental and occupational health and safety

laws and regulations. There can be no assurance that we are at all times in complete compliance

with all of these requirements. We have made and will continue to make capital and other

expenditures to comply with environmental regulations. If additional laws and regulations are

enacted in the future, which restrict our ability to manufacture and market our products, including

our treated lumber products, it could adversely affect our sales and profits. If existing laws are

interpreted differently, it could also increase our financial costs.

Seasonality and weather conditions could adversely affect us. Some aspects of our business are

seasonal in nature and results of operations vary from quarter to quarter. Our treated lumber and

outdoor specialty products, such as fencing, decking, and lattice, experience the greatest seasonal

effects. Sales of treated lumber, primarily consisting of Southern Yellow Pine, also experience

the greatest Lumber Market risk (see “Historical Lumber Prices” in Management’s Discussion and

Analysis of Financial Condition and Results of Operations which is presented under Item 7 of this

Form 10-K and is incorporated herein by reference). Treated lumber sales are generally at their

highest levels between April and August. This sales peak, combined with capacity constraints in

the wood treatment process, requires us to build our inventory of treated lumber throughout the

winter and spring. (This also has an impact on our receivables balances, which tend to be

significantly higher at the end of the second and third quarters.) Because sales prices of treated

lumber products may be indexed to the Lumber Market at the time they are shipped, our profits can

be negatively affected by prolonged declines in the Lumber Market during our primary selling

season. To mitigate this risk, consignment inventory programs are negotiated with certain vendors

that are intended to decrease our exposure to the Lumber Market by correlating the purchase price

of the material with the related sell price to the customer. These programs include those

materials which are most susceptible to adverse changes in the Lumber Market.

The majority of our products are used or installed in outdoor construction activities; therefore,

short-term sales volume, our gross margins, and our profits can be negatively affected by adverse

weather conditions, particularly in our first and fourth quarters. In addition, adverse weather

conditions can negatively impact our productivity and costs per unit.

8

New preservatives will be developed to treat our products. The manufacturers of preservatives

continue to develop new preservatives. All of our wood preservation facilities utilize either Amine

Copper Quaternary (“ACQ”), ProWood® Micro or borates. While we believe treated products

are reasonably priced relative to alternative products such as composites or vinyl, consumer

acceptance may be impacted which would in turn affect our future operating results. In addition,

new preservatives could increase our cost of treating products in the future.

Market conditions for the supply of certain lumber products and inbound transportation may be

limited. These conditions, which occur on occasion, have resulted in difficulties procuring

desired quantities and receiving orders on a timely basis for all industry participants. We are not

certain how these conditions may impact our short-term sales volumes and profitability. However,

we attempt to mitigate the risks of these conditions by:

| • |

|

Our pricing practices (see “Impact of the Lumber Market on Our Operating Results” in Management’s Discussion and

Analysis of Financial Condition and Results of Operations which is presented under Item 7 of this Form 10-K and is

incorporated herein by reference); |

| |

| • |

|

Leveraging our size with mill and transportation suppliers to ensure they achieve supply and service requirements; |

| |

| • |

|

Increasing our utilization of consigned inventory programs with mills; and |

| |

| • |

|

Expanding our supply base of dedicated carriers. |

Item 1B. Unresolved Staff Comments.

Not applicable.

Item 2. Properties.

Our corporate headquarters building is located in suburban Grand Rapids, Michigan. We currently

have approximately 90 facilities located throughout the United States, Canada, and Mexico.

Depending upon function and location, these facilities typically utilize office space,

manufacturing space, treating space and covered storage.

We own all of our properties, free from any significant mortgage or other encumbrance, except for

approximately 20 regional facilities which are leased. We believe all of these operating

facilities are adequate in capacity and condition to service existing customer locations.

Item 3. Legal Proceedings.

Information regarding our legal proceedings is set forth in Note M of our Consolidated Financial

Statements which are presented under Item 8 of this Form 10-K and are incorporated herein by

reference.

9

Item 4. Submission of Matters to a Vote of Security Holders.

Not applicable.

Additional Item: Executive Officers of the Registrant.

The following table lists the names, ages, and positions of our executive officers as of February

1, 2008. Executive officers are elected annually by the Board of Directors at the first meeting of

the Board following the annual meeting of shareholders.

| |

|

|

|

|

|

|

| Name |

|

Age |

|

Position |

William G. Currie

|

|

|

60 |

|

|

Executive Chairman, Universal Forest Products, Inc. |

Michael B. Glenn

|

|

|

56 |

|

|

President and Chief Executive Officer, Universal Forest Products, Inc. |

C. Scott Greene

|

|

|

52 |

|

|

President, Universal Forest Products Eastern Division, Inc. |

Patrick M. Webster

|

|

|

48 |

|

|

President, Universal Forest Products Western Division, Inc. |

Robert D. Coleman

|

|

|

53 |

|

|

Executive Vice President of Manufacturing, Universal Forest Products, Inc. |

Matthew J. Missad

|

|

|

47 |

|

|

Executive Vice President and Secretary, Universal Forest Products, Inc. |

Michael R. Cole

|

|

|

41 |

|

|

Chief Financial Officer and Treasurer, Universal Forest Products, Inc. |

Ronald G. Klyn

|

|

|

50 |

|

|

Chief Information Officer, Universal Forest Products, Inc. |

Joseph F. Granger

|

|

|

42 |

|

|

Executive Vice President of Sales and Marketing, Universal Forest Products, Inc. |

William G. Currie joined us in 1971. From 1983 to 1990, Mr. Currie was President of Universal

Forest Products, Inc., and he was the President and Chief Executive Officer of The Universal

Companies, Inc. from 1989 until the merger to form Universal Forest Products, Inc. in 1993. On

January 1, 2000, Mr. Currie also became Vice Chairman of the Board. On April 19, 2006, Mr. Currie

became Executive Chairman.

Michael B. Glenn joined us in 1974. In June of 1989, Mr. Glenn was elected Senior Vice President

of our Southwest Operations, and on December 1, 1997, became President of Universal Forest

Products Western Division, Inc. Effective January 1, 2000, Mr. Glenn was promoted to President

and Chief Operating Officer. On July 1, 2006, Mr. Glenn became Chief Executive Officer.

C. Scott Greene joined us in 1991. In November of 1996 he became General Manager of Operations

for our Florida Region, and in January of 1999 became Vice President of Marketing for Universal

Forest Products, Inc. During early 2000, Mr. Greene became President of Universal Forest Products

Eastern Division, Inc.

Patrick M. Webster joined us in 1985. He has held various sales, purchasing and management

positions throughout his career with us. Mr. Webster became Vice President of the Far West Region

in 1999, and on July 1, 2007, became President of Universal Forest Products Western Division, Inc.

10

Robert D. Coleman, joined us in 1979. Mr. Coleman was promoted to Senior Vice President of our

Midwest Operations in September 1993. On December 1, 1997, Mr. Coleman became the Executive Vice

President of Manufacturing of the Universal Forest Products Eastern Division, Inc. On January 1,

1999, Mr. Coleman was named the Executive Vice President of Manufacturing.

Matthew J. Missad joined us in 1985. Mr. Missad has served as General Counsel and Secretary since

December 1, 1987, and Vice President Corporate Compliance since August 1989. In February 1996,

Mr. Missad was promoted to Executive Vice President.

Michael R. Cole, CPA, CMA, joined us in 1993. In January of 1997, Mr. Cole was promoted to

Director of Finance, and on January 1, 2000 was made Vice President of Finance and Treasurer. On

July 19, 2000, Mr. Cole became Chief Financial Officer.

Ronald G. Klyn joined us in 1993 as Information Services Manager. In October of 1999, Mr. Klyn was

promoted to Chief Information Officer.

Joseph F. Granger joined us in 1988. In 1997 he became Vice President of the Atlantic Region, in

2002 he became Regional Vice President of the Southeast Region, and on January 1, 2007, he became

Executive Vice President of Sales and Marketing.

PART II

The following information items in this Part II, which are contained in the 2007 Annual Report, are

specifically incorporated by reference into this Form 10-K Report. These portions of the 2007

Annual Report that are specifically incorporated by reference are filed as Exhibit 13 with this

Form 10-K Report.

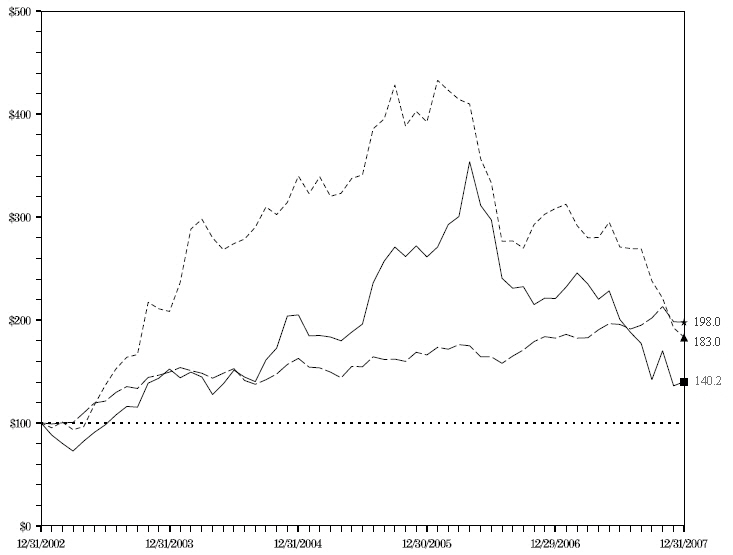

Item 5. Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer

Purchases of Equity Securities.

| (a) |

|

The information relating to market, holders and dividends is incorporated by reference from

the 2007 Annual Report under the caption “Price Range of Common Stock and Dividends.” |

| |

| |

|

There were no recent sales of unregistered securities. |

| |

| (b) |

|

Not applicable. |

| |

| (c) |

|

Issuer purchases of equity securities during the fourth quarter. |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fiscal Month |

|

(a) |

|

|

(b) |

|

|

(c) |

|

|

(d) |

|

September 30 – November 3, 2007(1) |

|

|

60,300 |

|

|

$ |

31.24 |

|

|

|

60,300 |

|

|

|

1,298,710 |

|

November 4 – December 1, 2007 |

|

|

42,000 |

|

|

$ |

30.39 |

|

|

|

42,000 |

|

|

|

1,256,710 |

|

December 2 – 29, 2007 |

|

|

12,000 |

|

|

$ |

28.68 |

|

|

|

12,000 |

|

|

|

1,244,710 |

|

11

|

|

|

| (a) |

|

Total number of shares purchased. |

| |

| (b) |

|

Average price paid per share. |

| |

| (c) |

|

Total number of shares purchased as part of publicly announced plans or

programs. |

| |

| (d) |

|

Maximum number of shares that may yet be purchased under the plans or programs. |

| |

| (1) |

|

On November 14, 2001 the Board of Directors approved a share repurchase

program (which succeeded a previous program) allowing us to repurchase up to 2.5

million shares of our common stock. As of December 29, 2007, the cumulative total of

authorized shares available for repurchase is 1.2 million shares. |

Item 6. Selected Financial Data.

The information required by this Item is incorporated by reference from the 2007 Annual Report

under the caption “Selected Financial Data.”

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of

Operations.

The information required by this item is incorporated by reference from the 2007 Annual Report

under the caption “Management’s Discussion and Analysis of Financial Condition and Results of

Operations.”

Item 7A. Quantitative and Qualitative Disclosures about Market Risk.

We are exposed to market risks related to fluctuations in interest rates on our variable rate debt,

which consists of a revolving credit facility and industrial development revenue bonds. We do not

currently use interest rate swaps, futures contracts or options on futures, or other types of

derivative financial instruments to mitigate this risk.

For fixed rate debt, changes in interest rates generally affect the fair market value, but not

earnings or cash flows. Conversely, for variable rate debt, changes in interest rates generally do

not influence fair market value, but do affect future earnings and cash flows. We do not have an

obligation to prepay fixed rate debt prior to maturity, and as a result, interest rate risk and

changes in fair market value should not have a significant impact on such debt until we would be

required to refinance it.

On December 29, 2007, the estimated fair value of our long-term debt, including the current

portion, was $207.6 million, which was $1.5 million greater than the carrying value. The estimated

fair value is based on rates anticipated to be available to us for debt with similar terms and

maturities. The estimated fair value of notes payable included in current liabilities and the

revolving credit facility approximated the carrying values.

12

Expected cash flows over the next five years related to debt instruments are as follows:

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

2008 |

|

|

2009 |

|

|

2010 |

|

|

2011 |

|

|

2012 |

|

|

Thereafter |

|

|

Total |

|

($US equivalents, in thousands) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Long-term Debt: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fixed Rate ($US) |

|

|

|

|

|

$ |

15,000 |

|

|

|

|

|

|

|

|

|

|

$ |

118,500 |

|

|

|

|

|

|

$ |

133,500 |

|

Average interest rate |

|

|

|

|

|

|

5.63 |

% |

|

|

|

|

|

|

|

|

|

|

6.70 |

% |

|

|

|

|

|

|

|

|

Variable Rate ($US) |

|

$ |

945 |

|

|

$ |

317 |

|

|

$ |

271 |

|

|

$ |

254 |

|

|

$ |

54,884 |

|

|

$ |

15,900 |

|

|

$ |

72,571 |

|

Average interest rate(1) |

|

|

5.71 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (1) |

|

Average of rates at December 29, 2007. |

Item 8. Financial Statements and Supplementary Data.

The information required by this Item is incorporated by reference from the 2007 Annual Report

under the following captions:

| |

“Management’s Annual Report on Internal Control Over Financial Reporting” |

“Report of Independent Registered Public Accounting Firm on Internal Control Over Financial

Reporting” |

“Report of Independent Registered Public Accounting Firm” |

“Consolidated Balance Sheets” |

“Consolidated Statements of Earnings” |

“Consolidated Statements of Shareholders’ Equity” |

“Consolidated Statements of Cash Flows” |

“Notes to Consolidated Financial Statements” |

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial

Disclosure.

Not applicable.

Item 9A. Controls and Procedures.

| (1) |

|

Evaluation of Disclosure Controls and Procedures. With the participation of

management, our chief executive officer and chief financial officer, after evaluating the

effectiveness of our disclosure controls and procedures (as defined in Exchange Act Rules 13a

— 15e and 15d — 15e) as of the year ended December 29, 2007 (the “Evaluation Date”), have

concluded that, as of such date, our disclosure controls and procedures were effective. |

| |

| (2) |

|

Management’s Annual Report on Internal Control Over Financial Reporting.

Management’s Annual Report on Internal Control Over Financial Reporting is included in the

2007 Annual Report under the caption “Management’s Annual Report on Internal Control Over

Financial Reporting” and is incorporated herein by reference. Our accounting firm’s

attestation Report on our internal control over financial reporting is also included in the

2007 Annual Report in the caption “Report of Independent Registered Public Accounting Firm on

Internal Control Over Financial Reporting” and is incorporated herein by reference. |

13

| (3) |

|

Changes in Internal Controls. During the fourth quarter ended December 29, 2007,

there were no changes in our internal control over financial reporting that materially

affected, or is reasonably likely to materially affect, our internal control over financial

reporting. |

Item 9B. Other Information.

Not applicable.

PART III

Item 10. Directors, Executive Officers and Corporate Governance.

Information relating to our directors, compliance with Section 16(a) of the Securities and Exchange

Act of 1934 and various corporate governance matters is incorporated by reference from our

definitive Proxy Statement for the year ended December 29, 2007 for the 2008 Annual Meeting of

Shareholders, as filed with the Commission (“2008 Proxy Statement”), under the captions “Election

of Directors,” “Corporate Governance and Board Matters,” and “Section 16(a)

Beneficial Ownership Reporting Compliance.” Information relating to executive officers is included

in this report in the last Section of Part I under the caption “Additional Item: Executive Officers

of the Registrant.” Information relating to our code of ethics is included in this report in Part

I, Item 1 under the caption “Available Information”.

Item 11. Executive Compensation.

Information relating to director and executive compensation is incorporated by reference from the

2008 Proxy Statement under the caption “Executive Compensation.” The “Compensation Committee

Report” included in the 2008 Proxy Statement is incorporated hereby by reference for the purpose of

being furnished herein and is not and shall not be deemed to be filed under the Securities Exchange

Act of 1934, as amended.

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related

Shareholder Matters.

Information relating to security ownership of certain beneficial owners and management is

incorporated by reference from our 2008 Proxy Statement under the captions “Ownership of Common

Stock” and “Securities Ownership of Management.”

14

Information relating to securities authorized for issuance under equity compensation plans as of

December 29, 2007, is as follows:

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

Number of shares |

|

| |

|

|

|

|

|

|

|

|

|

remaining |

|

| |

|

|

|

|

|

|

|

|

|

available for future |

|

| |

|

Number of |

|

|

Weighted |

|

|

issuance under |

|

| |

|

shares to be |

|

|

average |

|

|

equity |

|

| |

|

issued upon |

|

|

exercise |

|

|

compensation |

|

| |

|

exercise of |

|

|

price of |

|

|

plans [excluding |

|

| |

|

outstanding |

|

|

outstanding |

|

|

shares reflected in |

|

| |

|

options |

|

|

options |

|

|

column (a)] |

|

| |

|

(a) |

|

|

(b) |

|

|

(c) |

|

| |

Equity compensation plans approved by security holders |

|

|

796,477 |

|

|

$ |

20.92 |

|

|

|

987,603 |

|

Equity compensation plans not approved by security

holders |

|

none |

|

|

|

|

|

|

|

|

|

Item 13. Certain Relationships and Related Transactions, and Director Independence.

Information relating to certain relationships and related transactions, and director independence

is incorporated by reference from the 2008 Proxy Statement under the captions “Election of

Directors”, “Affirmative Determination Regarding Director Independence and Other Matters” and

“Related Party Transactions.”

Item 14. Principal Accounting Fees and Services.

Information relating to the types of services rendered by our Independent Auditors and the fees

paid for these services is incorporated by reference from our 2008 Proxy Statement under the

caption “Independent Public Accountants — Fees and Services.”

PART IV

Item 15. Exhibits, Financial Statement Schedules.

| (a) |

|

1. Financial Statements. The following are incorporated by reference, under

Item 8 of this report, from the 2007 Annual Report: |

Management’s Annual Report on Internal Control Over Financial Reporting

Report of Independent Registered Public Accounting Firm on Internal Control Over Financial Reporting

Report of Independent Registered Public Accounting Firm

Consolidated Balance Sheets

Consolidated Statements of Earnings

Consolidated Statements of Shareholders’ Equity

Consolidated Statements of Cash Flows

Notes to Consolidated Financial Statements

15

2.

Financial Statement Schedules. All schedules required by this Form 10-K

Report have been omitted because they were inapplicable, included in the Consolidated

Financial Statements or Notes to Consolidated Financial Statements, or otherwise not required

under instructions contained in Regulation S-X.

3.

Exhibits. Reference is made to the Exhibit Index which is included in this

Form 10-K Report.

(b) Reference is made to the Exhibit Index which is included in this Form 10-K Report.

(c) Not applicable.

16

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities and Exchange Act of

1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned,

thereunto duly authorized.

| |

|

|

|

|

| Dated: February 26, 2008 |

UNIVERSAL FOREST PRODUCTS, INC.

|

|

| |

By: |

/s/ Michael B. Glenn

|

|

| |

|

Michael B. Glenn, Chief Executive Officer |

|

| |

| |

and |

|

| |

|

|

|

|

| |

/s/ Michael R. Cole

|

|

| |

Michael R. Cole, Chief Financial Officer |

|

| |

and Treasurer |

|

17

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been

signed below on this 26th day of February, 2008, by the following persons on behalf of us and in

the capacities indicated.

Each Director whose signature appears below hereby appoints Matthew J. Missad and Michael R.

Cole, and each of them individually, as his attorney-in-fact to sign in his name and on his behalf

as a Director, and to file with the Commission any and all amendments to this report on Form 10-K

to the same extent and with the same effect as if done personally.

| |

|

|

/s/ Peter F. Secchia

|

|

/s/ William G. Currie |

|

|

|

Peter F. Secchia, Director

|

|

William G. Currie, Director |

|

|

|

/s/ Dan M. Dutton

|

|

/s/ John M. Engler |

|

|

|

Dan M. Dutton, Director

|

|

John M. Engler, Director |

|

|

|

/s/ John W. Garside

|

|

/s/ Michael B. Glenn |

|

|

|

John W. Garside, Director

|

|

Michael B. Glenn, Director |

|

|

|

/s/ Gary F. Goode

|

|

/s/ Mark A. Murray |

|

|

|

Gary F. Goode, Director

|

|

Mark A. Murray, Director |

|

|

|

/s/ Louis A. Smith |

|

|

|

|

|

18

EXHIBIT INDEX

| |

|

|

|

|

| Exhibit # |

|

Description |

| |

| 3 |

|

Articles of Incorporation and Bylaws. |

|

|

|

|

|

|

|

(a)

|

|

Registrant’s Articles of Incorporation were filed as Exhibit 3(a) to a

Registration Statement on Form S-1 (No. 33-69474) and the same is incorporated

herein by reference. |

|

|

|

|

|

|

|

(b)

|

|

Registrant’s Bylaws were filed as Exhibit 3(b) to a Registration

Statement on Form S-1 (No. 33-69474) and the same is incorporated herein by

reference. |

|

|

|

|

|

| 4 |

|

Instruments Defining the Rights of Security Holders. |

|

|

|

|

|

|

|

(a)

|

|

Specimen form of Stock Certificate for Common Stock was filed as

Exhibit 4(a) to a Registration Statement on Form S-1 (No. 33-69474) and the same is

incorporated herein by reference. |

|

|

|

|

|

| 10 |

|

Material Contracts. |

|

|

|

|

|

|

|

*(a)(3)

|

|

Consulting Agreement with Peter F. Secchia, dated December 31, 2002, and

Assignment dated January 1, 2003 was filed as Exhibit 10(a)(3) to a Form 10-K,

Annual Report for the year ended December 28, 2002 and the same is incorporated

herein by reference. |

|

|

|

|

|

|

|

*(a)(4)

|

|

Nondisclosure and Non-Compete Agreement with Peter F. Secchia, dated December

31, 2002 was filed as Exhibit 10(a)(4) to a Form 10-K, Annual Report for the year

ended December 28, 2002 and the same is incorporated herein by reference. |

|

|

|

|

|

|

|

*(a)(5)

|

|

Conditional Share Grant Agreement with William G. Currie dated April 17, 2002

was filed as Exhibit 10(a)(5) to a Form 10-K, Annual Report for the year ended

December 28, 2002 and the same is incorporated herein by reference. |

|

|

|

|

|

|

|

*(a)(6)

|

|

Form of Conditional Share Grant Agreement utilized under the Company’s Long Term

Stock Incentive Plan, was filed as Exhibit 10(a) to a Form 10-Q Quarterly Report

for the quarter ended September 25, 2004 and the same is incorporated herein by

reference. |

|

|

|

|

|

|

|

*(a)(7)

|

|

Consulting and Non-Compete Agreement with William G. Currie, dated December 17,

2007. |

E-1

| |

|

|

|

|

| Exhibit # |

|

Description |

|

|

|

|

| |

|

|

*(a)(8)

|

|

Employment, Consulting (and Non-Competition) Agreement with Robert K. Hill,

dated June 15, 2007. |

|

|

|

|

|

|

|

|

|

|

|

(b)

|

|

Form of Indemnity Agreement entered into between the Registrant and

each of its directors was filed as Exhibit 10(b) to a Registration Statement on

Form S-1 (No. 33-69474) and the same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

*(e)(1)

|

|

Form of Executive Stock Option Agreement was filed as Exhibit 10(e)(1) to a

Registration Statement on Form S-1 (No. 33-69474) and the same is incorporated

herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

*(e)(2)

|

|

Form of Officers’ Stock Option Agreement was filed as Exhibit 10(e)(2) to a

Registration Statement on Form S-1 (No. 33-69474) and the same is incorporated

herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

*(f)

|

|

Salaried Employee Bonus Plan was filed as Exhibit 10(f) to a

Registration Statement on Form S-1 (No. 33-69474) and the same is incorporated

herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(i)(4)

|

|

Series 2004-A, Credit Agreement dated December 20, 2004 was filed as Exhibit

10(i) to a Form 8-K Current Report dated December 21, 2004 and the same is

incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(i)(5)

|

|

First Amendment dated February 12, 2007 relating to Series 2004-A, Credit

Agreement dated December 20, 2004 was filed as Exhibit 10(i) to a Form 8-K Current

Report dated February 15, 2007 and the same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(j)(1)

|

|

Series 1998-A, Senior Note Agreement dated December 21, 1998 was filed as Exhibit

10(j)(1) to a Form 10-K Annual Report for the year ended December 26, 1998, and the

same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(j)(2)

|

|

Series 2002-A, Senior Note Agreement dated December 18, 2002 was filed as Exhibit

10(j)(2) to a Form 10-K Annual Report for the year ended December 28, 2002 and the

same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(k)(4)

|

|

Program for Accounts Receivable Transfer (“PARTS”) Agreement dated March 7, 2006

was filed as Exhibit 10(k)(4) to a Form 10-K Annual Report for the year ended

December 31, 2005 and the same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

| 13 |

|

Selected portions of the Company’s Annual Report to Shareholders for the fiscal year ended

December 29, 2007. |

E-2

| |

|

|

|

|

| Exhibit # |

|

Description |

|

|

| |

| 14 |

|

Code of Ethics for Senior Financial Officers |

|

|

|

|

|

|

|

|

|

(a)

|

|

Code of Ethics for Chief Financial Officer was filed as Exhibit 14(a)

to a Form 10-K, Annual Report for the year ended December 25, 2004 and the same is

incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(b)

|

|

Code of Ethics for Vice President of Accounting and Administration was

filed as Exhibit 14(a) to a Form 10-K, Annual Report for the year ended December

25, 2004 and the same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

|

|

(c)

|

|

Code of Ethics for Vice President of Accounting was filed as Exhibit

14(c) to a Form 10-K, Annual Report for the year ended December 31, 2005 and the

same is incorporated herein by reference. |

|

|

|

|

|

|

|

|

|

| 21 |

|

Subsidiaries of the Registrant. |

|

|

|

|

|

|

|

| 23 |

|

Consent of Ernst & Young LLP. |

|

|

|

|

|

|

|

| 31 |

|

Certifications. |

|

|

|

|

|

|

|

|

|

(a)

|

|

Certificate of the Chief Executive Officer of Universal Forest

Products, Inc., pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 (18

U.S.C. 1350). |

|

|

|

|

|

|

|

|

|

|

|

(b)

|

|

Certificate of the Chief Financial Officer of Universal Forest

Products, Inc., pursuant to Section 302 of the Sarbanes-Oxley Act of 2002 (18

U.S.C. 1350). |

|

|

|

|

|

|

|

|

|

32

|

|

Certifications. |

|

|

|

|

|

|

|

|

|

|

|

|

|

(a)

|

|

Certificate of the Chief Executive Officer of Universal Forest

Products, Inc., pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 (18

U.S.C. 1350). |

|

|

|

|

|

|

|

|

|

|

|

(b)

|

|

Certificate of the Chief Financial Officer of Universal Forest

Products, Inc., pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 (18

U.S.C. 1350). |

|

|

| |

|

|

|

| * |

|

Indicates a compensatory arrangement. |

E-3

Filed by Bowne Pure Compliance

Exhibit 10(a) (7)

NONDISCLOSURE AND NON-COMPETE AGREEMENT

This Agreement is entered into as of the 17th day of December, 2007, by and between Universal

Forest Products, Inc., and its affiliates and subsidiaries, 2801 East Beltline NE, Grand Rapids, MI

49525 (herein “UFP”), and William G. Currie, an individual, of 1830 Beard Drive SE, Grand Rapids,

MI 49546 (herein “Currie”).

RECITALS

| A. |

|

Currie intends to retire as an officer of UFP as of July 21, 2009. UFP wishes to restrict

his services from being provided to any competitors of UFP. |

The Parties agree as follows:

SECTION 1. DISCLOSURE OF INFORMATION.

Currie acknowledges that UFP’s trade secrets, private or secret processes as they exist from

time to time, and information concerning customers and their identity, products, developments,

manufacturing techniques, new product plans, equipment, inventions, discoveries, patent

applications, ideas, designs, engineering drawings, sketches, renderings, other drawings,

manufacturing and test data, computer programs, progress reports, materials, costs, specifications,

processes, methods, research, procurement and sales activities and procedures, promotion and

pricing techniques, and credit and financial data concerning customers of UFP, as well as

information relating to the management, operation, or planning of UFP, herein the (“Proprietary

Information”) are valuable, special, and unique assets of UFP, access to and knowledge of which may

be essential to the performance of Currie’s duties under this Agreement. In light of the highly

competitive nature of the industries in which UFP conducts businesses, Currie agrees that all

Proprietary Information obtained by Currie as a result of its relationship with UFP shall be

considered confidential. In recognition of this fact, Currie agrees that except as may be

necessary for UFP’s benefit, in Currie’s reasonable judgment, Currie will not, during and after the

Non-Compete Period, disclose any of such Proprietary Information to any person or entity for any

reason or purpose whatsoever without the written consent of UFP, and Currie will not make use of

any Proprietary Information for Currie’s own purposes or for the benefit of any other person or

entity (except UFP) under any circumstances.

SECTION 2. NON-COMPETITION AGREEMENT.

In order to further protect the confidentiality of the Proprietary Information and in

recognition of the highly competitive nature of the industries in which UFP conducts its

businesses, and for the consideration set forth herein, Currie further agrees that during

and for the period commencing on July 21, 2009 and ending on July 21, 2012 (the “Non-Compete

Period”):

2.1 Currie will not directly or indirectly engage in any Business Activities (hereinafter

defined), other than on behalf of UFP, whether such engagement is as an officer, director,

proprietor, employee, partner, investor (other than as a holder of less than 1% of the outstanding

capital stock of a publicly-traded corporation), advisor, agent, or other participant, in any

geographic area in which the products or services of UFP have been distributed or provided during

the period of Currie’s consulting relationship with UFP. For purposes of this Agreement, the term

“Business Activities” shall mean the design, development, manufacture, sale, marketing, or

servicing of UFP’s products, together with all other activities engaged in by UFP or any of its

subsidiaries at any time during Currie’s relationship with UFP, and activities in any way related

to activities with respect to which Currie renders consulting services under this Agreement.

2.2 Currie will not directly or indirectly engage in any of the Business Activities (other

than on behalf of UFP) by supplying products or providing services to any customer with whom UFP

has done any business during the consulting relationship with UFP, whether such engagement is as an

officer, director, proprietor, employee, partner, investor (other than as a holder of less than one

percent (1%) of the outstanding capital stock of a publicly traded corporation), advisor, agent, or

other participant.

2.3 Assistance to Others. Currie will not directly or indirectly assist others in

engaging in any of the Business Activities in any manner prohibited to Currie under this Agreement.

2.4 UFP’s Employees. Currie will not directly or indirectly induce employees of UFP

to engage in any activity hereby prohibited to Currie or to terminate their employment with UFP.

2.5 Non-Compete Payments. In exchange for Currie’s agreements and obligations under

this Section 2, Currie will receive a payment of Forty One Thousand Six Hundred Sixty Six Dollars

($41,666.00) per month for the term of the Non-Compete Period, subject to earlier termination upon

the death or Disability of Currie. Disability shall mean a physical or mental injury or illness

that totally and permanently renders Currie unable to perform all of the functions called for under

this Agreement.

2

SECTION 3. INTERPRETATION.

Although Currie and UFP consider the restrictions contained in Sections 1 and 2 of this

Agreement reasonable for the purpose of preserving the goodwill, proprietary rights, and going

concern value of UFP, if a final judicial determination is made by a court

having jurisdiction that the time or territory or any other restriction contained in Section 2

is an unenforceable restriction on the activities of Currie, the provisions of such restriction

shall not be rendered void but shall be deemed amended to apply as to such maximum time and

territory and to such other extent as such court may judicially determine or indicate to be

reasonable. Alternatively, if the court referred to above finds that any restriction contained in

Section 2 or any remedy provided in Section 4 of this Agreement is unenforceable, and such

restriction or remedy cannot be amended so as to make it enforceable, such finding shall not affect

the enforceability of any of the other restrictions contained in this Agreement or the availability

of any other remedy. The provisions of Sections 1 and 2 shall in no respect limit or otherwise

affect the obligations of Currie under other agreements with UFP.

SECTION 4. REMEDIES.

Currie acknowledges and agrees that UFP’s remedy at law for a breach or threatened breach of

any of the provisions of Sections 1 and 2 of this Agreement would be inadequate and, in recognition

of this fact, in the event of a breach or threatened breach by Currie of any of the provisions of

Sections 1 and 2, Currie agrees that, in addition to its remedies at law, at UFP’s option, all

rights of Currie, and obligations of UFP, under this Agreement may be terminated. UFP shall be

entitled to equitable relief in the form of specific performance, temporary restraining order,

temporary or permanent injunction, or any other equitable remedy which may then be available. UFP

shall not be required to post bond, and Currie agrees not to oppose UFP’s request for equitable

relief. Currie acknowledges that the granting of a temporary injunction, temporary restraining

order or permanent injunction merely prohibiting the use of Proprietary Information would not be an

adequate remedy upon breach or threatened breach of Sections 1 and 2, and consequently agrees upon

any such breach or threatened breach to the granting of injunctive relief prohibiting the design,

development, manufacture, marketing or sale of products and providing of services of the kind

designed, developed, manufactured, marketed, sold or provided by UFP or its subsidiaries during the

term of Currie’s relationship with UFP. Nothing contained in this Section 4 shall be construed as

prohibiting UFP from pursuing, in addition, any other remedies available to it for such breach or

threatened breach.

SECTION 5. MISCELLANEOUS PROVISIONS.

5.1 Assignment. This Agreement shall not be assignable by either party, except by UFP

to any subsidiary or affiliate of UFP (now or hereafter existing) or to any successor in interest

to UFP’s business, provided that in the case of an assignment to an affiliate or subsidiary, UFP

shall remain liable as a guarantor for payments due to Currie hereunder.

3

5.2 Binding Effect. The provisions of this Agreement shall be binding upon and inure

to the benefit of the heirs, personal representatives, successors, and assigns of the parties.

5.3 Notice. Any notice or other communication required or permitted to be given under

this Agreement shall be in writing and shall be mailed by certified mail, return receipt requested,

postage prepaid, addressed to the parties at the address stated on the first page of this

Agreement. The address of a party to which notices or other communications shall be mailed may be

changed from time to time by giving written notice to the other party.

5.4 Litigation Expense. In the event of a default under this Agreement, the

defaulting party shall reimburse the non-defaulting party for all costs and expenses reasonably

incurred by the non-defaulting party in connection with the default, including without limitation

reasonable attorney’s fees. The non-defaulting party may seek reimbursement in a court of competent

jurisdiction. Additionally, in the event a suit or action is filed to enforce this Agreement or

with respect to this Agreement, the prevailing party or parties shall be reimbursed by the other

party for all costs and expenses incurred in connection with the suit or action, including without

limitation reasonable attorney’s fees at the trial level and on appeal.

5.5 Waiver. No waiver of any provision of this Agreement shall be deemed, or shall

constitute, a waiver of any other provision, whether or not similar, nor shall any waiver

constitute a continuing waiver. No waiver shall be binding unless executed in writing by the party

making the waiver.

5.6 Applicable Law. This Agreement shall be governed by and shall be construed in

accordance with the laws of the State of Michigan.

5.7 Entire Agreement. This Agreement constitutes the entire Agreement between the

parties pertaining to its subject matter, and it supersedes all prior contemporaneous agreements,

representations, and understandings of the parties. No supplement, modification, or amendment of

this Agreement shall be binding unless executed in writing by all parties.

[SIGNATURES ON FOLLOWING PAGE.]

4

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

UNIVERSAL FOREST PRODUCTS, INC.: |

|

|

|

|

|

|

|

|

|

|

|

By:

|

|

/s/ Matthew J. Missad |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Its:

|

|

Executive Vice President |

|

|

|

|

|

|

|

|

|

| |

|

/s/ William G. Currie |

|

|

| |

|

|

|

|

| |

|

William G. Currie |

|

|

5

Filed by Bowne Pure Compliance

Exhibit 10(a) (8)

EMPLOYMENT, CONSULTING

(AND NON-COMPETITION) AGREEMENT

| |

|

|

|

|

DATE:

|

|

June 15, 2007 |

|

|

|

|

|

|

|

PARTIES:

|

|

Robert K. Hill

|

|

Universal Forest Products Western Div., Inc. |

|

|

5974 Watson Drive

|

|

(and its affiliates and subsidiaries) |

|

|

Fort Collins, CO 80528

|

|

2801 East Beltline NE |

|

|

(herein “Hill”

|

|

Grand Rapids, MI 49525 |

|

|

|

|

(herein “UFP” or the “Company”) |

The Parties agree as follows:

SECTION 1. RETIREMENT.

Hill is currently the President of Universal Forest Products Western Division, Inc. From June

15, 2007 to December 31, 2007, Hill shall remain an officer of UFP. The Company will appoint a new

President of Universal Forest Products Western Division, Inc., effective July 1, 2007. Effective

January 1, 2008 (the “Effective Date”), Hill shall be deemed to have resigned as an officer of the

Company and will become a consultant to the Company. As of the Effective Date, Hill releases UFP

from any employment obligations and wishes to enter into a consulting agreement as described in

this document.

SECTION 2. RETENTION OF HILL AS CONSULTANT.

2.1 Effective Date. As of the Effective Date, UFP shall retain Hill as an independent

contractor and consultant. Hill accepts such consulting relationship upon the terms and conditions

set forth in this Agreement.

2.2 Services. Hill agrees to provide sales, manufacturing and purchasing consulting

for the exclusive benefit of UFP. Hill shall perform such consulting services faithfully for UFP

during the term of this Agreement. The initial consulting services are listed on Appendix “A” and

may be amended in writing as agreed by the parties.

2.3 Condition Precedent. UFP’s obligations hereunder, including but not limited to

the Compensation described in Section 3 of this Agreement, are expressly conditioned upon the

execution of the Full and Final Release by Hill on or before December 31, 2007. The Full and Final

Release is attached as Appendix “B.”

1

SECTION 3. COMPENSATION.

3.1 Employment Compensation. For the period ended fiscal year 2007, Hill shall

receive his normal base salary, ROI bonus consisting of 25% of the Universal Forest Products

Western Division pool plus a portion of the discretionary pool (minimum 10% and maximum 25%), as

determined by Hill and the CEO, and officer benefits package.

3.2 Consulting Fee and Expense Reimbursement. On the Effective Date, in full

satisfaction for all consulting services rendered by Hill for UFP under this Agreement, UFP shall

pay Hill’s consulting business a consulting fee as follows:

(a) Thirty Thousand Three Hundred Fifty Two Dollars and 08/100 ($30,352.08) per month, in

exchange for up to two (2) days or twenty (20) hours per week. Some weeks may require more time,

and other weeks may require less time, as agreed by the parties.

(b) Hill and his spouse shall be eligible for COBRA continuation of medical benefits effective

January 1, 2008. The fee for standard salaried insurance will be paid by UFP for the 18 months of

COBRA coverage, or longer, if eligible. From July 1, 2009 through November 30, 2012, UFP shall pay

the premium for a Colorado Preferred Blue Cross policy, or its similarly priced equivalent, with a

reasonable deductible, for Hill and his spouse. Hill shall be responsible for all deductibles,

co-pays and policy limitations.

(c) After December 31, 2007, Hill will be responsible for all of Hill’s costs to perform the

obligations under this agreement. UFP will reimburse Hill for business telephone and internet

access used for UFP business as agreed by the CEO and Hill. If Hill is required by UFP to travel

to perform specific duties, UFP will reimburse the ordinary and necessary costs to travel and

perform such duties.

3.3 Other Compensation and Fringe Benefits. Except as set forth in this Agreement,

Hill shall not receive any other compensation from UFP or participate in or receive benefits under

any other UFP fringe benefit programs, including, without limitation, disability, life insurance,

bonus, and profit sharing benefits. On the Effective Date, Hill shall receive a one-time payment

of Five Thousand Dollars ($5,000.00).

SECTION 4. NATURE OF RELATIONSHIP; EXPENSES.

4.1 Independent Contractor. As of the Effective Date, Hill shall be an independent

contractor and shall not be the employee, servant, agent, partner, or joint venturer of UFP, or

any of its officers, directors, or consultants. Except as expressly provided herein, Hill

shall not have the right to or be entitled to any of the employee benefits of UFP or its

subsidiaries except as expressly agreed in writing. Hill has no authority to assume or create any

obligation or liability, express or implied, on UFP’s behalf or in its name or to bind UFP in any

manner whatsoever.

2

4.2 Insurance and Taxes. Hill agrees to arrange for Hill’s own liability, disability,

and workers’ compensation insurance, and that of Hill’s employees, if any. Hill agrees to be

responsible for Hill’s own tax obligations accruing as a result of payments for services rendered

under this Agreement, as well as for the tax withholding obligations with respect to Hill’s

employees, if any. It is expressly understood and agreed by Hill that should UFP for any reason

incur tax liability or charges whatsoever as a result of not making any withholdings from payments

for services under this Agreement, Hill will reimburse and indemnify UFP for the same. Hill agrees

to sign independent contractor agreement(s) containing terms sufficient to comply with Colorado and

Federal law regarding his status as an independent contractor.

4.3 Equipment, Tools, Consultants and Overhead. Except as set forth in this

Agreement, Hill shall provide, at his own expense, all equipment and tools needed to provide

services under this Agreement, including the salaries of and benefits provided to any employees of

Hill. Hill shall be responsible for all of Hill’s overhead costs and expenses.

SECTION 5. TERM.

5.1 Initial Term; Renewal. The consulting relationship under this Agreement shall

commence on the Effective Date and continue in effect until December 31, 2010. The parties may

mutually agree in writing to extend this Agreement.

5.2 Effect of Termination. Termination of the consulting relationship shall not

affect the provisions of Sections 6, 7 and 8, which provisions shall survive any termination in

accordance with their terms.

SECTION 6. DISCLOSURE OF INFORMATION.

Hill acknowledges that UFP’s trade secrets, private or secret processes as they exist from

time to time, and information concerning customers and their identity, products, developments,

manufacturing techniques, new product plans, equipment, inventions, discoveries, patent

applications, ideas, designs, engineering drawings, sketches, renderings, other drawings,

manufacturing and test data, computer programs, progress reports, materials,

costs, specifications, processes, methods, research, procurement and sales activities and

procedures, promotion and pricing techniques, and credit and financial data concerning customers of

UFP, as well as information relating to the management, operation, or planning of UFP, herein the

(“Proprietary Information”) are valuable, special, and unique assets of UFP, access to and

knowledge of which may be essential to the performance of Hill’s duties under this Agreement as an

employee or as a consultant.

3

In light of the highly competitive nature of the industry in which

UFP conducts business, Hill agrees that all Proprietary Information obtained by Hill as a result of

its relationship with UFP shall be considered confidential. In recognition of this fact, Hill

agrees that Hill will not, during and after the Consulting Period, disclose any of such Proprietary

Information to any person or entity for any reason or purpose whatsoever, and Hill will not make

use of any Proprietary Information for Hill’s own purposes or for the benefit of any other person

or entity (except UFP) under any circumstances. Notwithstanding anything herein to the contrary,

no obligation or liability shall accrue hereunder with respect to any of the Proprietary

Information to the extent that such Proprietary Information (1) is or becomes publicly available

other than as a result of acts by Hill in violation of this Agreement; or (2) is, on the advice of

counsel, required to be disclosed by law or legal process.

SECTION 7. NONCOMPETITION AGREEMENT.

In order to further protect the confidentiality of the Proprietary Information and in

recognition of the highly competitive nature of the industries in which UFP conducts its

businesses, and for the consideration set forth herein, Hill further agrees that during and for the

period June 15, 2007 and ending on December 31, 2010.

7.1 Hill will not directly or indirectly engage in any Business Activities (hereinafter

defined), other than on behalf of UFP, whether such engagement is as an officer, director,

proprietor, employee, partner, investor (other than as a holder of less than 1% of the outstanding